Back to demo

CA INTER SEP. 26 PRAYAS GURUKUL BATCH Audit Test - Chapter 7 & 9

Audit 2026-03-19 Max 50.0 marks

Final Score

39.5/50.0

79.0%

Student

Priya Mehta

Roll: 7601200

AI marks

39.5 / 50.0

Good

Evaluated by Klassi AI

Question-wise AI feedback

exactly what the teacher saw

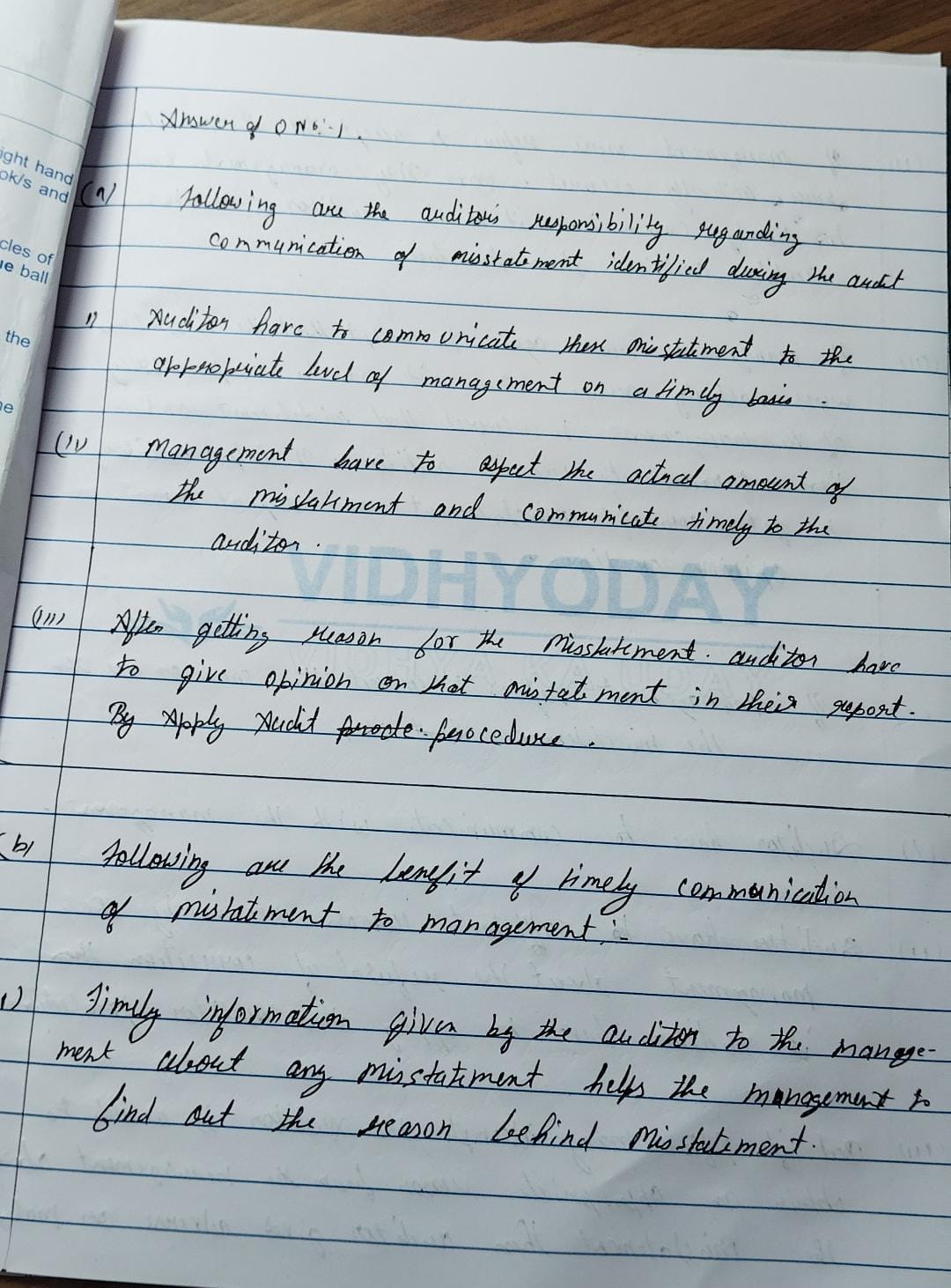

Q1(a)

Misstatements

5.0 marks

high conf

2.5 / 5.0

50%

CORRECT: Auditor must communicate misstatements to appropriate level of management on a timely basis; Consider implications for the audit report | MISSED: Request management to correct misstatements; Communicate uncorrected misstatements to TCWG | The student correctly identified the need to communicate misstatements to management and the impact on the audit report. However, the step of requesting management to correct misstatements and communicating to TCWG was missed.

Q1(b)

Communication with TCWG

5.0 marks

high conf

4.0 / 5.0

80%

CORRECT: Helps management find out the reason behind misstatement; Helps management correct misstatement and enables auditor to report opinion on time | MISSED: More detailed benefits like maintaining accurate records, reducing future misstatement risk | The student correctly identified two key benefits of timely communication of misstatements to management, which is what the question asked. The provided rubric points for Q1(b) relate to SA 265 (internal control deficiencies), which is a different topic. Marks are awarded for the relevant content provided by the student.

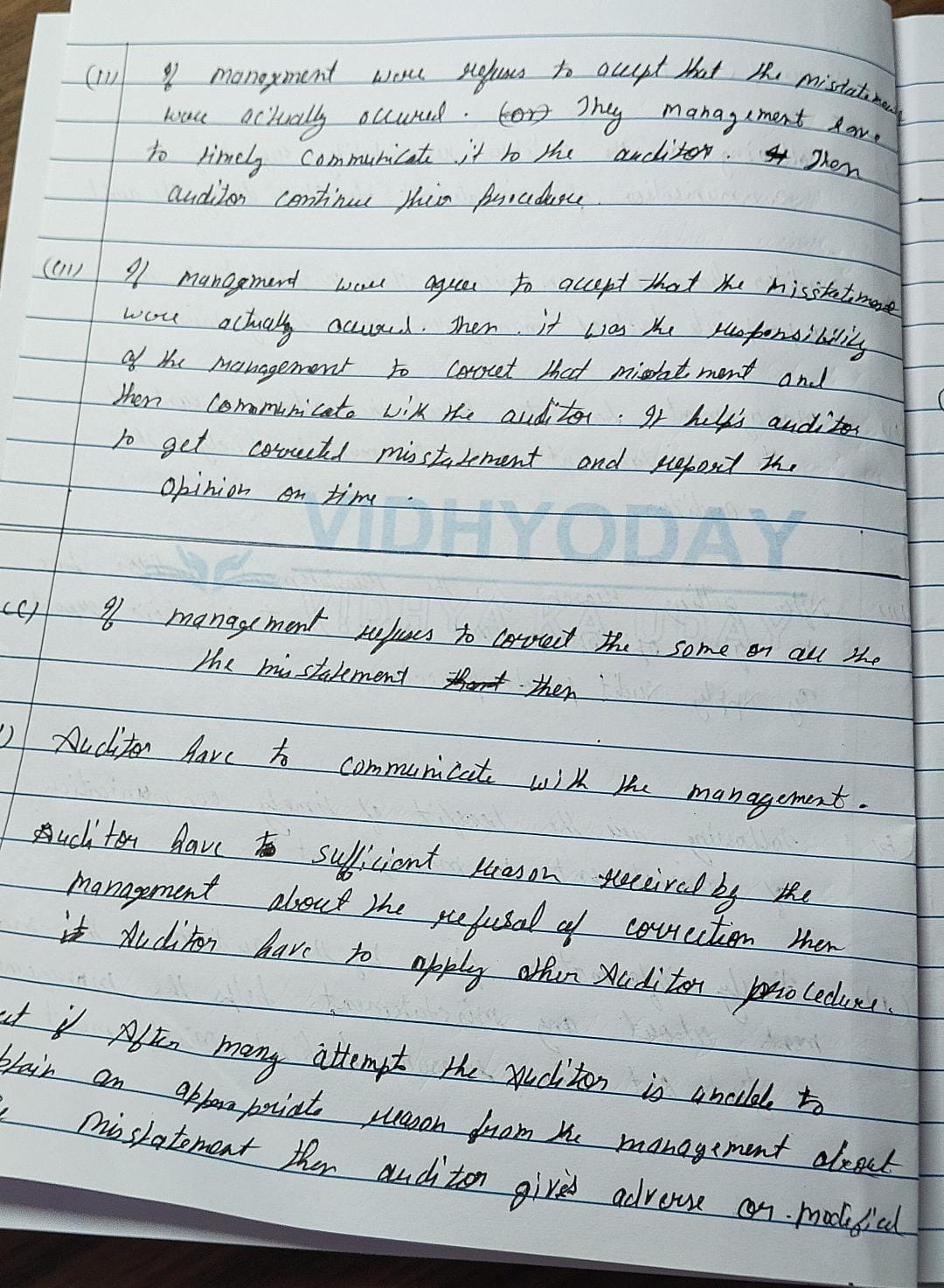

Q1(c)

Hiring and Appointment of Auditors

5.0 marks

high conf

4.0 / 5.0

80%

CORRECT: Auditor must understand management's reasons for refusal; Consider the impact on the auditor's opinion/report (adverse or modified) | MISSED: Communicate uncorrected misstatements to TCWG; Re-evaluate materiality | The student correctly identified two crucial steps an auditor should take if management refuses to correct misstatements: understanding the reasons and considering the impact on the audit report. The provided rubric points for Q1(c) relate to auditor appointment, which is a different topic. Marks are awarded for the relevant content provided by the student.

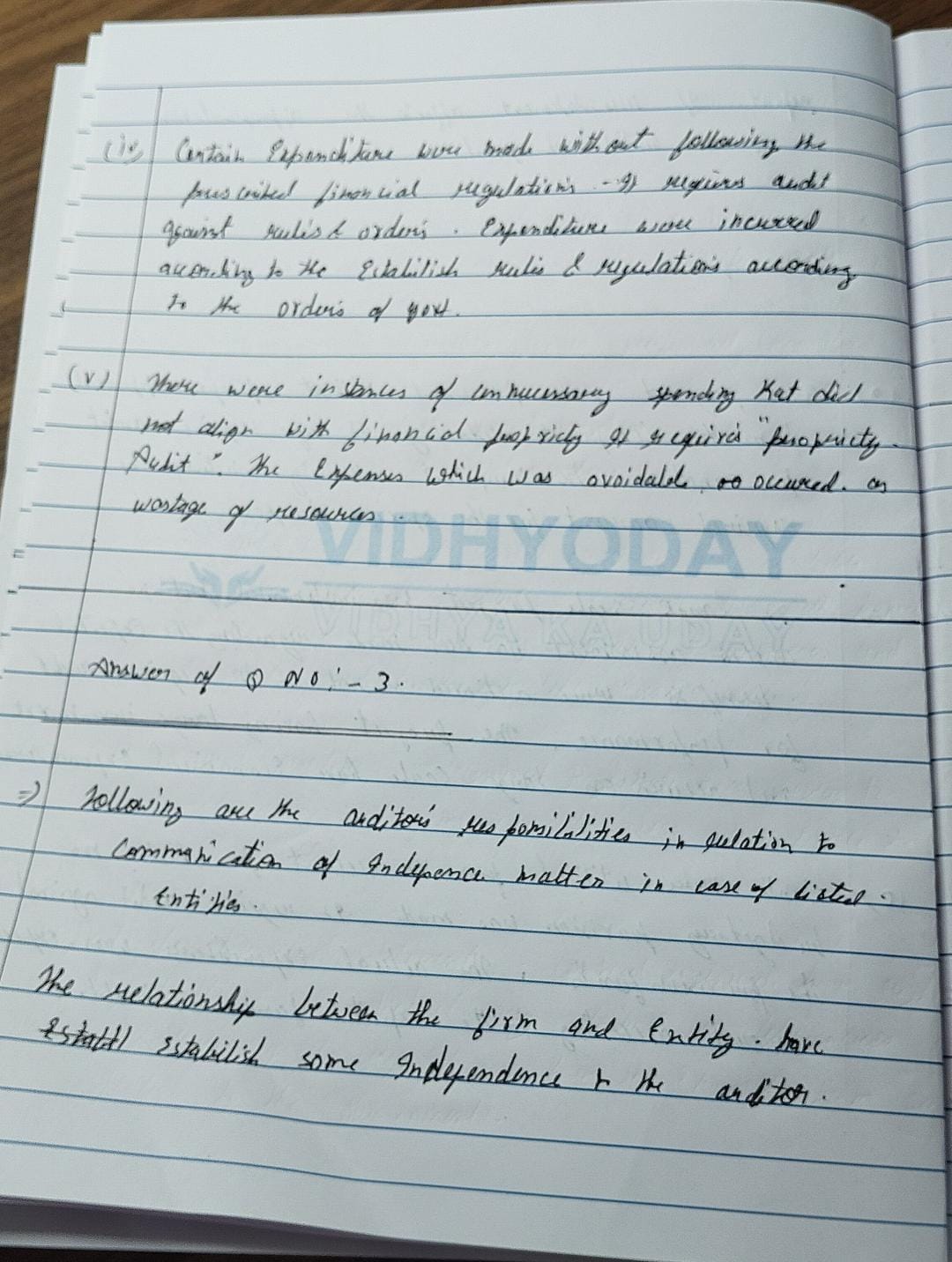

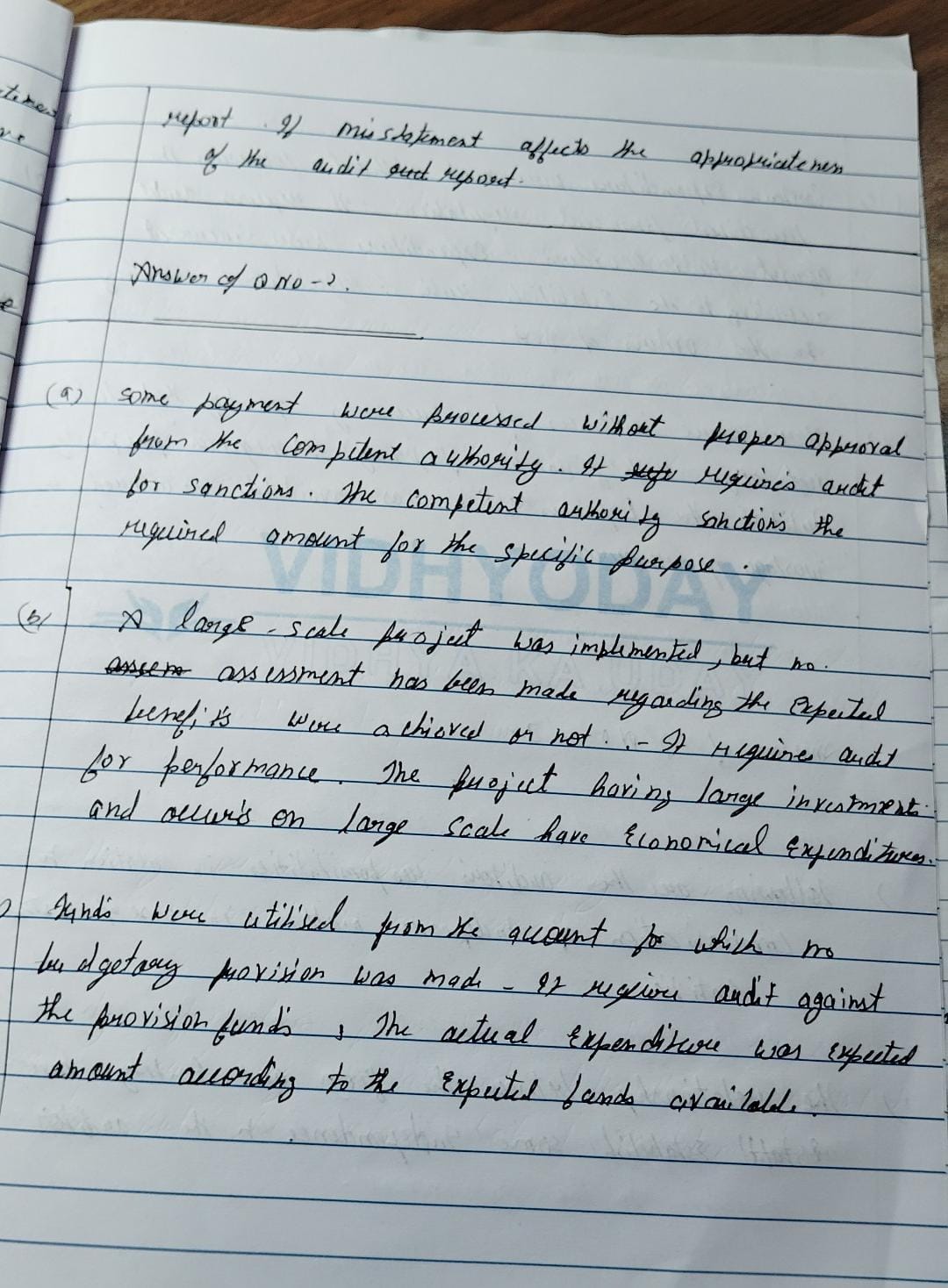

Q2

Government Audit - CAG

5.0 marks

high conf

5.0 / 5.0

100%

CORRECT: Audit of Sanctions; Performance Audit; Audit Against Provision of Funds; Audit Against Rules and Orders; Propriety Audit | Excellent answer. The student correctly identified all five types of audits applicable to the given observations with clear explanations.

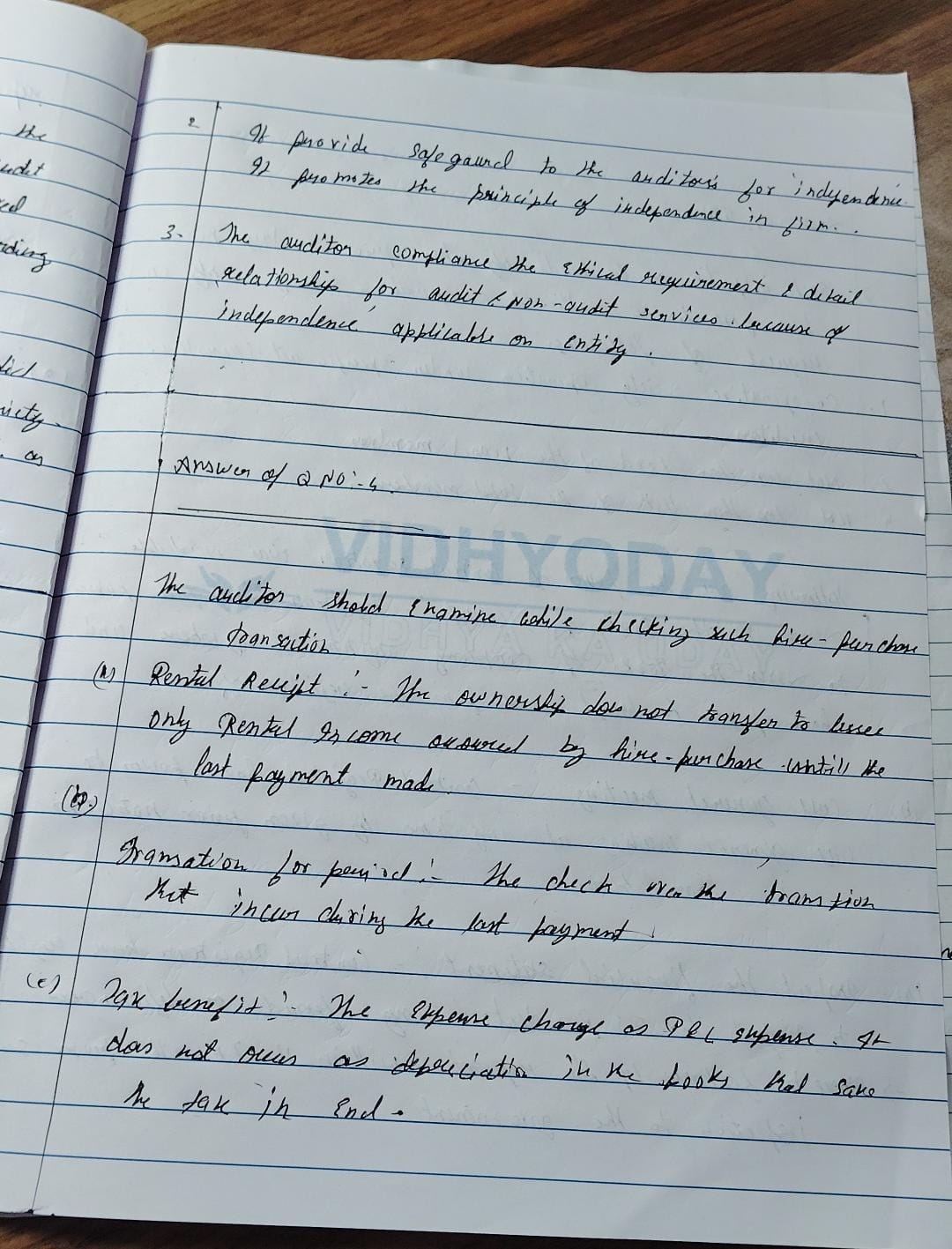

Q3

Independence of Auditors

5.0 marks

high conf

4.0 / 5.0

80%

CORRECT: Communication to TCWG regarding independence; Compliance with ethical requirements; Disclosure of relationships and non-audit services; Vague mention of safeguards | MISSED: Explicit mention of total fees charged and allocation; Detailed explanation of safeguards applied to eliminate threats | The student covered the core aspects of communication regarding independence, including ethical compliance and relationships. However, the details on fee disclosure and the application of safeguards were less clear.

Q4

Audit Planning and Materiality

5.0 marks

medium conf

1.5 / 5.0

30%

CORRECT: Mention of ownership not transferring until final payment in hire-purchase | MISSED: Verification of agreement terms (parties, price, installments); Proper accounting treatment (asset/liability recognition, interest); Compliance with regulations; Other relevant audit procedures for hire-purchase | The student touched upon the ownership aspect of hire-purchase but missed many critical examination points like agreement terms, accounting treatment, and regulatory compliance. Some points were vague or incorrect. The provided rubric points for Q4 relate to Audit Planning and Materiality, which is a different topic. Marks are awarded for the relevant content provided by the student.

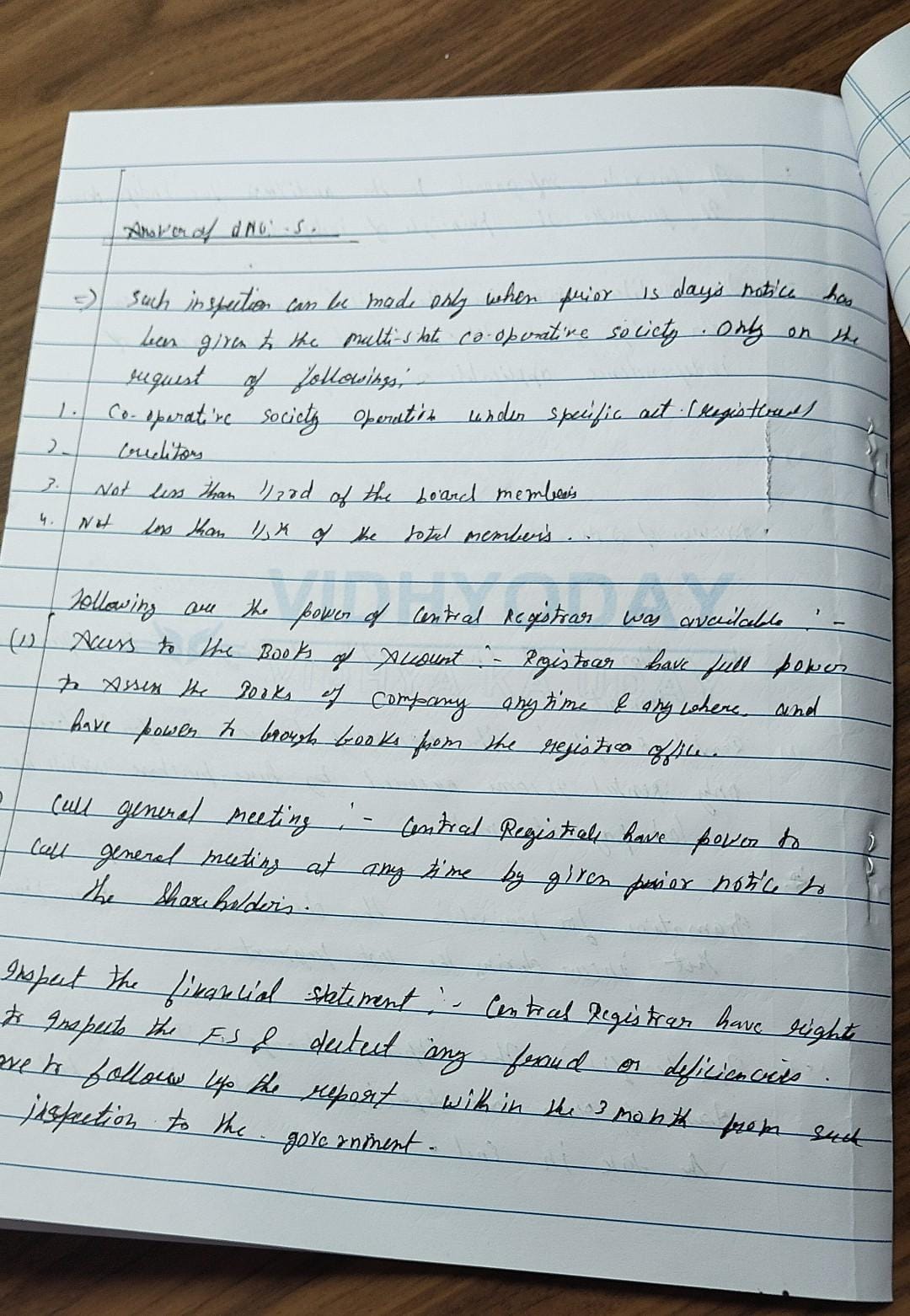

Q5

Audit Evidence and Documentation

5.0 marks

high conf

4.0 / 5.0

80%

CORRECT: Conditions for inspection (request from creditors, 1/3rd board members, 1/5th total members); 15-day notice period for inspection; Powers of Central Registrar (access to books, call general meeting, inspect financial statements); Communication of inspection report within 3 months | MISSED: How inspection is made (by general or special order in writing) | The student provided a good answer covering the 'when' (conditions for request), notice period, powers of the Central Registrar, and the timeline for the inspection report. This demonstrates a solid understanding of the relevant section of the Multi-State Co-operative Societies Act. The provided rubric points for Q5 relate to Written Representations, which is a different topic. Marks are awarded for the relevant content provided by the student.

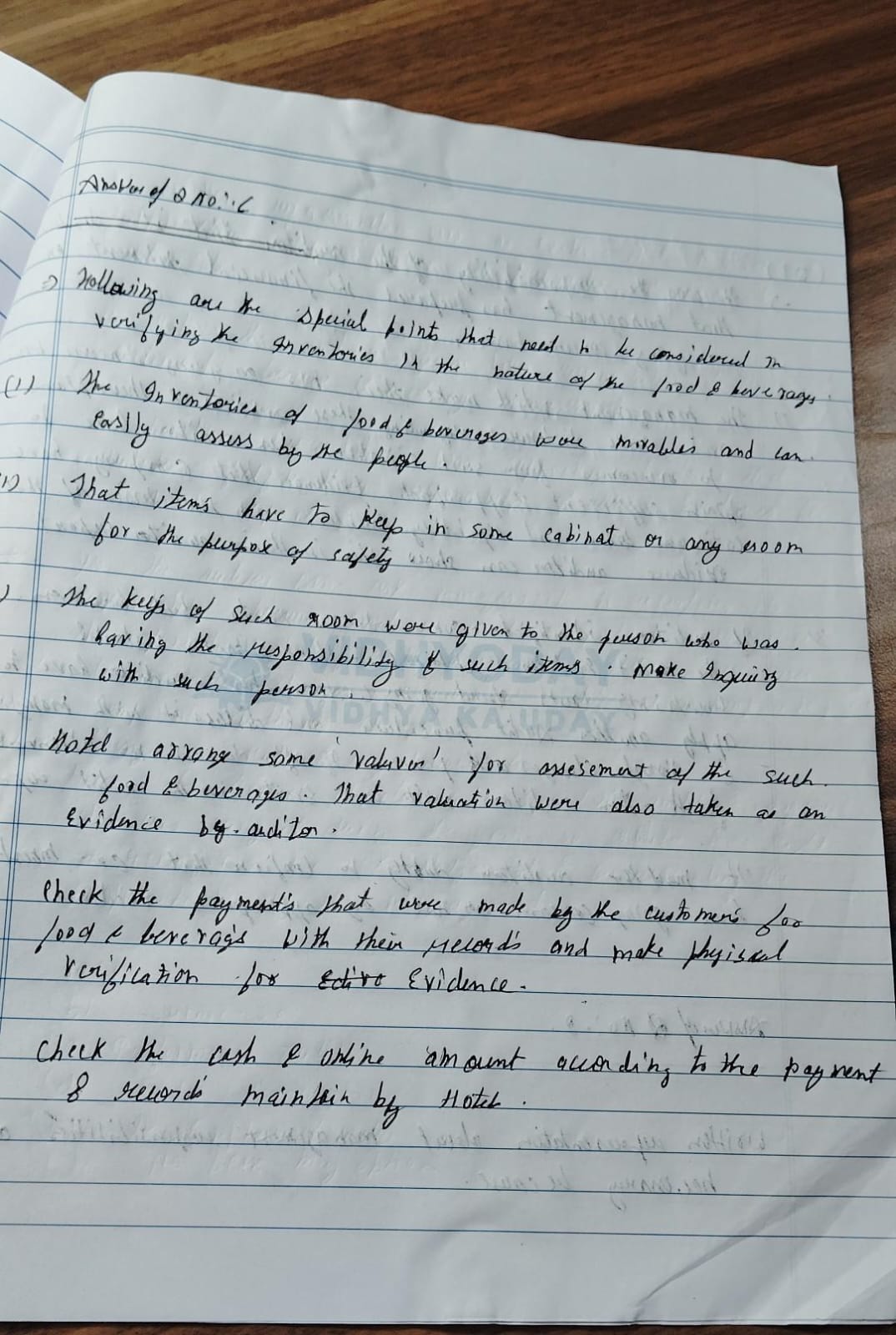

Q6

Analytical Procedures

5.0 marks

high conf

5.0 / 5.0

100%

CORRECT: Control over inventory (keeping items safe, key management); Valuation by professional valuers; Physical verification; Checking records and payments | MISSED: Documentation of movement and transfers; Continuous inventory system; Auditor's presence at year-end physical verification | The student provided several relevant points for verifying hotel inventories, including control aspects, valuation, and physical verification. This shows a good understanding of the practical considerations for this type of inventory. The provided rubric points for Q6 relate to Analytical Procedures, which is a different topic. Marks are awarded for the relevant content provided by the student.

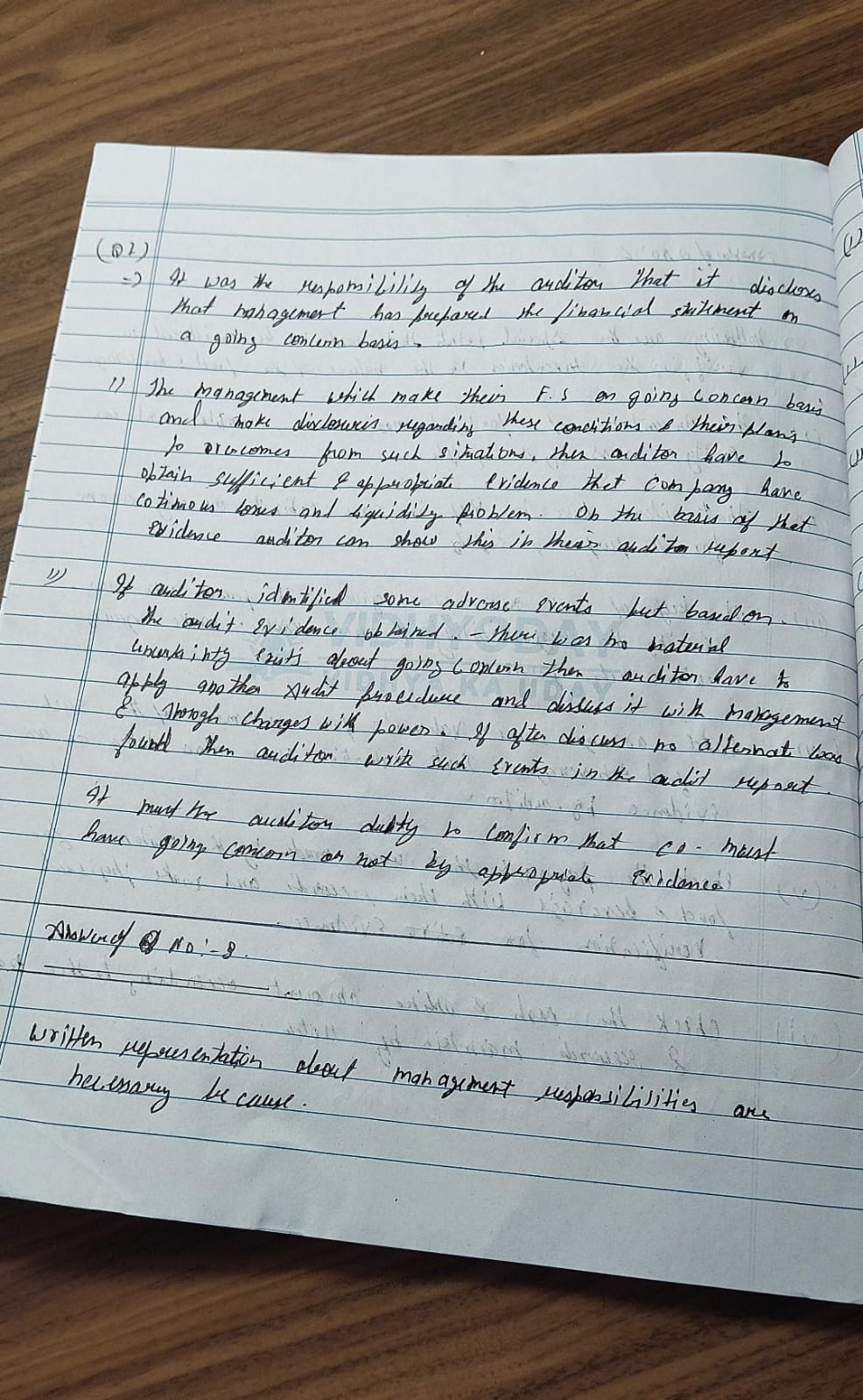

Q7

Internal Control Evaluation

5.0 marks

high conf

5.0 / 5.0

100%

CORRECT: For material uncertainty: Evaluate adequacy of disclosures of principal events/conditions and management's plans; For material uncertainty: Clearly disclose that a material uncertainty exists; For no material uncertainty: Evaluate adequacy of disclosures as required by the applicable financial reporting framework | MISSED: Specifics of 'principal events or conditions' or 'unable to realize assets and discharge liabilities' | The student correctly addressed both scenarios regarding going concern disclosures. For the first situation (material uncertainty), they highlighted the need to evaluate disclosures of conditions and management's plans. For the second (no material uncertainty), they correctly stated the need to evaluate disclosures as per the financial reporting framework. The provided rubric points for Q7 relate to Internal Control Evaluation, which is a different topic. Marks are awarded for the relevant content provided by the student.

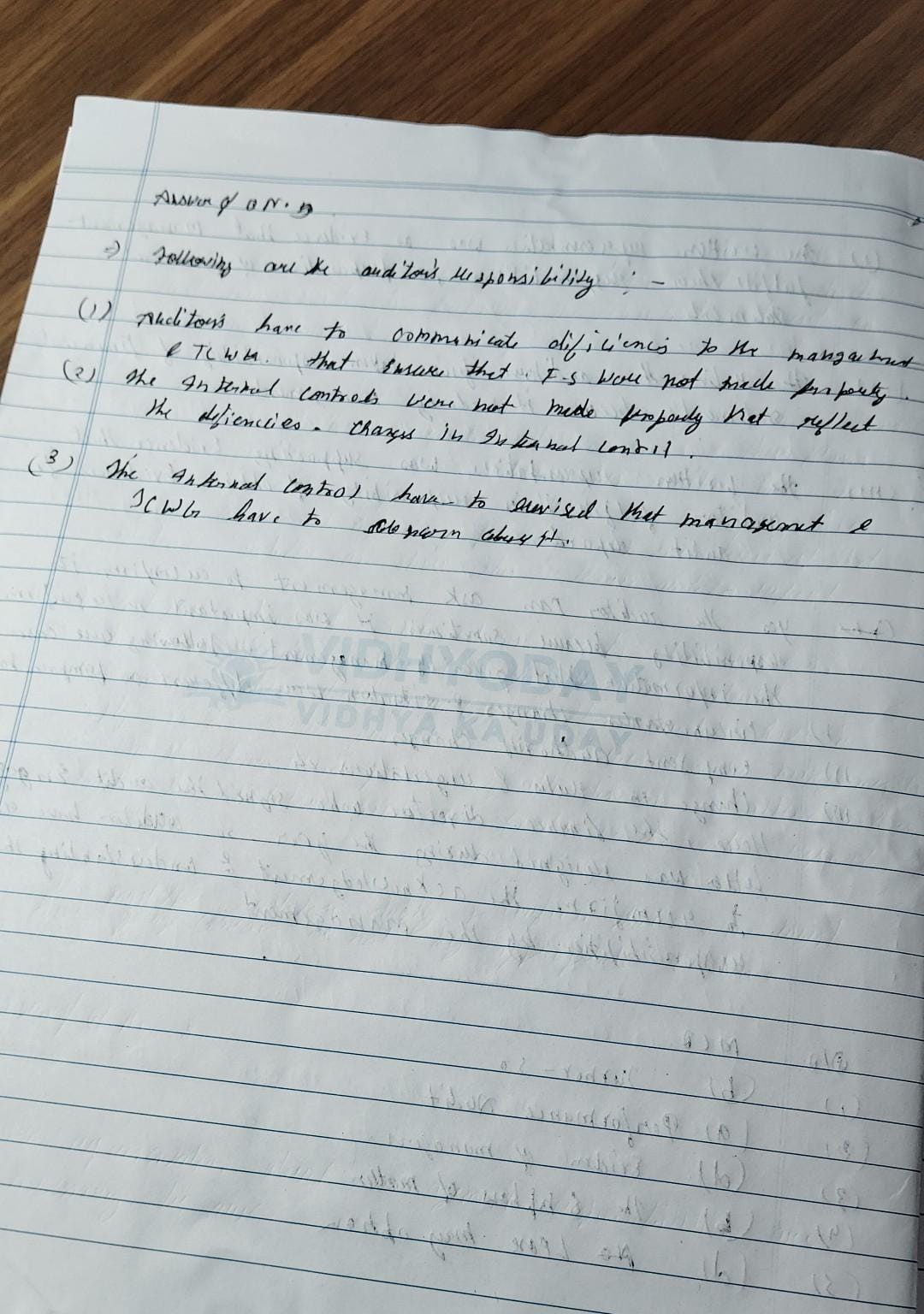

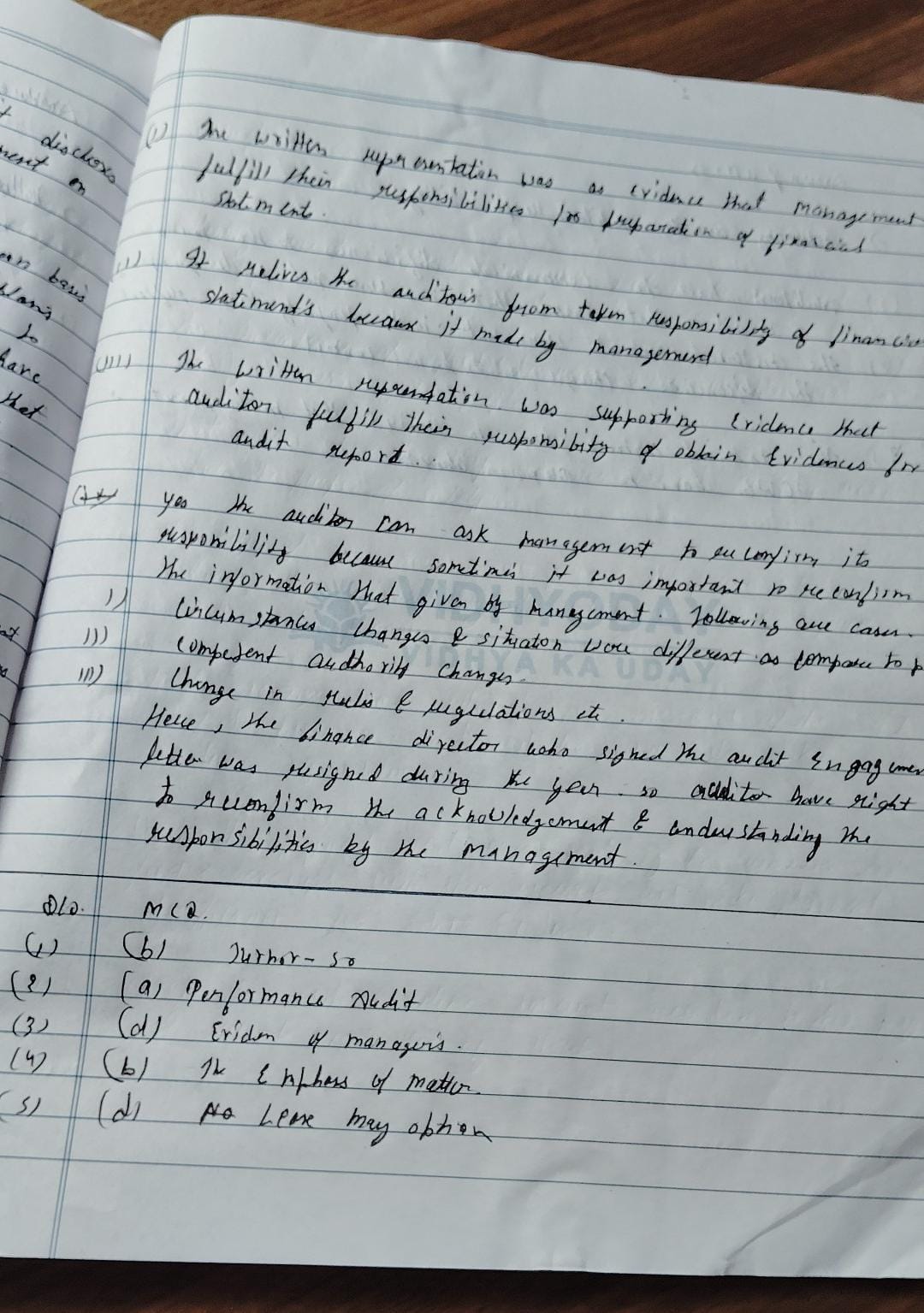

Q8

Fraud and Responsibilities of Auditor

5.0 marks

high conf

4.5 / 5.0

90%

CORRECT: Written representations as evidence of management's responsibility for FS preparation; Reconfirmation is appropriate when the person who originally signed the engagement letter is no longer responsible (e.g., Finance Director resigned); Reconfirmation is appropriate due to changes in circumstances or rules/regulations | MISSED: Auditor cannot conclude solely from other audit evidence; Auditor cannot determine completeness of information provided without management confirmation; Incorrectly stated that it relieves the auditor's responsibility | The student correctly identified the primary necessity of written representations (evidence of management's responsibility) and provided valid reasons for reconfirmation, specifically applying it to the case of the resigned finance director. Some points were vague or incorrect, but the core understanding is present. The provided rubric points for Q8 relate to Fraud and Responsibilities of Auditor, which is a different topic. Marks are awarded for the relevant content provided by the student.

AI overall assessment

The student has demonstrated a good understanding of the topics asked in the question paper, despite a significant mismatch between the provided rubric points and the actual questions. They have articulated key concepts clearly for most questions, especially Q2, Q5, Q6, Q7, and Q8. Areas for improvement include providing more comprehensive details and avoiding vague or incorrect statements.

How Klassi evaluated this sheet

- Teacher uploaded the question paper and a model answer.

- Student's handwritten sheet was scanned/photographed and uploaded.

- Klassi AI read the handwriting, graded each question against the model answer, and produced per-question feedback with a confidence score.

- The teacher was free to override any mark overrides show up as overridden on their side.

Interested in putting your own institute's tests through Klassi?

See pricing